Every Thursday afternoon in Bbuliro, fifteen women gather under a shade with their savings boxes and ledger books. They count contributions, approve loans to members, and celebrate each other’s small victories. This simple gathering has transformed their lives. Children who were dropping out of school are now graduating, medical emergencies no longer mean selling family assets, and small businesses are flourishing where there was only subsistence farming before.

This is the power of a Village Savings and Loan Association, or VSLA. It’s one of the most effective tools for financial inclusion in rural Uganda, and it’s something your community can start with nothing more than commitment, trust, and proper guidance.

At Rural Development Foundation, we’ve supported hundreds of VSLAs across the Greater Masaka region. We’ve seen these groups become the foundation of community transformation, lifting entire villages out of poverty through collective action and mutual support. In this comprehensive guide, we’ll show you exactly how to start and run a successful VSLA in your community.

In this guide, you’ll discover:

- What a VSLA is and why it works so effectively in rural communities

- The complete step-by-step process for starting a VSLA in Uganda

- Essential roles, rules, and structures that ensure success

- How to manage savings, loans, and record-keeping effectively

- Common challenges and practical solutions from experienced groups

- How VSLAs connect to larger financial opportunities through RDF

- Real success stories from the Masaka-region VSLAs

📥 Download this roadmap as a PDF: 7 Steps Roadmap to Starting Your VSLA by RDF Uganda (PDF)

Print and share with your community leaders | High-resolution version for meetings and workshops.

Understanding VSLAs: The Foundation of Community Finance

What Is a VSLA?

A Village Savings and Loan Association is a self-managed group of 15-30 people who save money together and provide small loans to members from their collective savings. Unlike traditional banks or microfinance institutions, VSLAs are entirely member-owned and member-managed. Every shilling comes from members, and every benefit goes back to members.

The Simple VSLA Cycle:

Members meet regularly (usually on a weekly or bi-weekly basis) to contribute their savings. These savings accumulate in a secure lockbox. Members can borrow from the collective savings pool and repay with a small interest. At the end of the cycle (typically 9-12 months), all savings plus accumulated interest are distributed back to members proportionally based on their contributions. Then the cycle begins again.

Why VSLAs Work So Well in Rural Uganda

Traditional banking often fails rural communities. Banks require documentation many people don’t have, impose minimum balances that exclude the poor, and locate branches far from villages. VSLAs solve all these problems by bringing financial services directly to the community, managed by the community, for the community.

Key Advantages of VSLAs:

- No Barriers to Entry: Anyone can join regardless of literacy level or employment status

- Builds Savings Discipline: Regular contributions create the habit of saving

- Immediate Access to Credit: Members can borrow when they need it without external approval

- Develops Financial Skills: Members learn budgeting, record-keeping, and loan management

- Creates Social Capital: Groups provide support, encouragement, and accountability

- Generates Returns: Interest from loans means members earn more than they saved

- Completely Transparent: All money and records are visible to all members

Pro Tip From the Field: Our community officers consistently observe that VSLA members develop financial confidence that carries over into all areas of their lives. Women who were afraid to enter a bank become group treasurers managing thousands of shillings. Men who never kept records become meticulous loan officers.

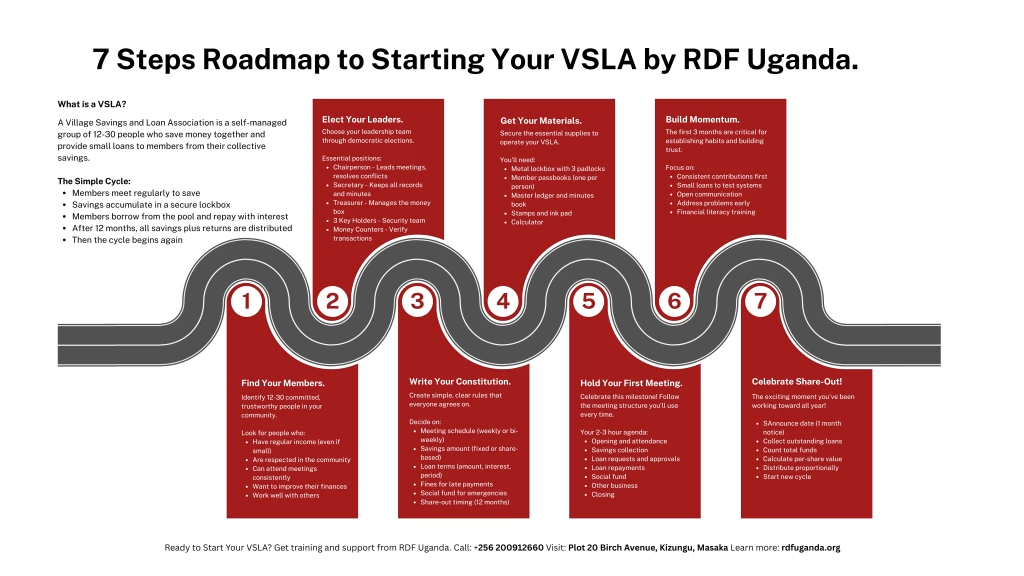

The Step-by-Step Process for Starting a VSLA in Uganda

Step 1: Identify Interested Community Members (Week 1)

Starting a VSLA in Uganda begins with finding the right people. You need 15-30 individuals who are committed, trustworthy, and willing to work together over the long term. VSLAs work best when members share common interests or live in the same area.

How to Recruit Members:

Start by talking with people you trust, neighbours, church members, or farming and market cooperative colleagues. Explain the VSLA concept and gauge interest. Look for people who:

- Have some regular income (even if small)

- Are respected in the community

- Can commit to attending regular meetings

- Are interested in improving their financial situation

- Can work cooperatively with others

Initial Meeting Agenda:

Gather interested people for an introductory meeting. Explain what a VSLA is, how it works, and what commitment is required. Be honest about both benefits and responsibilities. Answer questions and address concerns. At the end of this meeting, ask for firm commitments from those ready to proceed.

Step 2: Establish Group Identity and Leadership (Week 2)

Once you have committed members, formalize your group identity. Choose a name that reflects your community or aspirations. Many groups choose names like “Unity Savings Group,” “Progress Together,” or “Women of Hope.”

Elect Leadership Positions:

Every successful VSLA needs clear leadership. Hold elections for these essential positions:

Chairperson: Leads meetings, resolves conflicts, and represents the group externally. Should be respected, fair, and decisive.

Secretary: Keeps all records, including attendance, savings, loans, and meeting minutes. Requires basic literacy and numeracy skills.

Treasurer: Manages the money box, counts contributions, and distributes loans. Must be completely trustworthy and good with numbers.

Key Holders (3 people): Each holds one key to the lockbox, which requires all three keys to open. This prevents theft and ensures transparency.

Money Counters (2-3 people): Verify all transactions during meetings to ensure accuracy.

Hold democratic elections with secret ballots if needed. Make sure every member feels the leadership is fair and trustworthy.

Step 3: Develop Your VSLA Constitution (Weeks 2-3)

Your constitution is the rulebook that governs your VSLA. It should be simple, clear, and agreed upon by all members. Discuss and agree on these essential elements:

Meeting Schedule: When and where will you meet? Most VSLAs meet weekly or bi-weekly. Choose a day and time when most members can attend consistently.

Savings Amounts: How much will members save each meeting? Common approaches include:

- Fixed amount (everyone saves the same, e.g., 5,000 shillings)

- Share-based system (members can buy 1-5 shares per meeting, with each share worth a set amount like 2,000 shillings)

The share-based system offers more flexibility for members with varying incomes.

Loan Terms: Define your lending rules:

- Maximum loan amount (typically 2-3 times a member’s savings)

- Loan period (usually 1-3 months)

- Interest rate (commonly 5-10% per cycle, not per month)

- Repayment schedule (weekly or monthly)

- Late payment penalties

Fines and Penalties: Establish consequences for late arrival, missed meetings, or late loan repayment. Keep fines reasonable, the goal is accountability, not punishment.

Social Fund: Many VSLAs create a separate social fund through small contributions to help members during emergencies like funerals, medical crises, or fires.

Share-Out Timing: When will you distribute accumulated savings? Most groups choose 12 months to align with the agricultural cycle or major expense periods like school opening.

Write down all agreed-upon rules clearly. If possible, have each member sign or thumbprint the constitution to show commitment.

Pro Tip From the Field: Keep your initial rules simple and adjust as you learn. Many new VSLAs make rules too complicated and then struggle to follow them. Start basic and add detail as needed.

Step 4: Secure Essential Materials (Week 3)

You’ll need some basic supplies to operate your VSLA:

Lockbox: A metal box with three separate padlocks. This can be purchased or crafted by a local metalworker. Budget approximately 35,000-100,000 shillings for a quality box.

Ledger Books: Three main books are essential:

- Member Passbook (one per member to track individual savings and loans)

- Master Ledger (tracks all group transactions)

- Minutes Book (records meeting proceedings)

Stamps and Ink Pad: For authenticating entries in passbooks and ledgers

Calculator: For accurate counting during meetings

Chairs/Mats: For a comfortable meeting space

Many VSLAs fund these initial materials through special contributions from members or support from organisations like RDF. The total startup cost is typically 100,000-200,000 shillings divided among all members.

Step 5: Conduct Your First Savings Meeting (Week 4)

Your first official savings meeting is a milestone worth celebrating. Follow this structure, which you’ll repeat at every meeting:

1. Opening (10 minutes):

- Chairperson calls the meeting to order

- Opening prayer or moment of reflection

- Review the agenda for the meeting

2. Attendance and Fines (5 minutes):

- Secretary records attendance

- Collect fines from late arrivals

3. Previous Meeting Review (10 minutes):

- The secretary reads the previous minutes

- Treasurer reports current balance

- Address any outstanding issues

4. Savings Collection (30 minutes):

- Members come forward one by one

- State how many shares they’re buying this meeting

- Money counters verify each contribution

- The treasurer places money in the lockbox

- The secretary records the amount in the master ledger and member’s passbook

- Both books are stamped to authenticate

5. Loan Requests and Approvals (30 minutes):

- Members requesting loans present their cases

- State loan amount, purpose, and proposed repayment plan

- Group discusses and votes on each request

- Approved loans are disbursed immediately

- Loan terms recorded in the borrower’s passbook and master ledger

6. Loan Repayments (20 minutes):

- Borrowers make scheduled repayments

- Money counters verify amounts

- Payments are recorded in passbooks and the master ledger

- Late payments are addressed according to the constitution

7. Social Fund (10 minutes):

- Collect social fund contributions if applicable

- Discuss and approve any emergency requests

- Maintain separate records for the social fund

8. Other Business (15 minutes):

- Discuss group matters

- Plan upcoming activities

- Address member concerns

9. Closing (5 minutes):

- Recap decisions made

- Confirm next meeting date

- Closing prayer or reflection

Allow 2-3 hours for complete meetings initially. As your group gains experience, you’ll move more efficiently.

Step 6: Maintain Momentum Through Regular Cycles (Ongoing)

The first three months are crucial for establishing habits and building trust. During this period:

Build Savings: Focus on consistent contributions before lending heavily. Many successful groups spend the first 4-6 weeks just saving to build a lending pool.

Start with Small Loans: Initial loans should be modest to test your systems and build confidence. As the group matures, larger loans become possible.

Communicate Constantly: Encourage members to share challenges early. Financial difficulties, family issues, or concerns about group management should be addressed immediately before they become crises.

Educate Continuously: Use meeting time occasionally for financial literacy topics. RDF offers free training sessions on budgeting, business planning, and agricultural finance for VSLAs.

Step 7: Conduct Your First Share-Out (Month 12)

Share-out is the exciting culmination of your savings cycle. This is when all accumulated savings plus interest are distributed back to members proportionally.

Share-Out Process:

- Announce Share-Out Date: Give members at least one month’s notice

- Collect All Outstanding Loans: All loans must be repaid before the share-out

- Final Accounting: Verify all records are accurate and balanced

- Calculate Total Funds: Count all the money in the lockbox

- Determine Share Value: Divide total funds by total shares saved

- Distribute Proportionally: Each member receives payment based on their shares

- Celebrate: This is a significant achievement worth recognising

After the share-out, most groups immediately begin a new cycle with refreshed energy and higher savings targets.

Real Impact Story: The Bukinda-Kakintu Women’s VSLA completed their first cycle with 42 million shillings accumulated from 15 members. Each member received an average return of 135% on their savings, which went toward school fees, home improvements, and business investments. They immediately started cycle two with doubled weekly savings targets.

Essential VSLA Management Practices

Record-Keeping That Works

Good records are the foundation of VSLA success and trust. Follow these principles:

Double-Entry System: Every transaction appears in both the master ledger and the relevant member passbook. This creates accountability and prevents errors.

Immediate Recording: Write down transactions as they happen, not later. Memory fails, but written records don’t.

Verification: Money counters should verify and sign all transactions. Multiple eyes prevent mistakes and fraud.

Stamp Everything: Use your group stamp on all entries to prevent later additions or alterations.

Regular Audits: Every few months, conduct a full audit where all money is counted and verified against records. Invite respected community members to witness.

Managing Loans Effectively

Lending is where VSLAs provide the most value, but it’s also where problems can arise. Follow these guidelines:

Clear Loan Purposes: Borrowers should state specifically what they’ll use money for. Productive loans (for business or farming) generally work better than consumption loans.

Realistic Repayment: Ensure repayment schedules match borrowers’ income cycles. A farmer borrowing for inputs needs repayment aligned with harvest, not monthly payments she can’t make.

Group Guarantee: Many successful VSLAs require borrowers to identify other members who guarantee the loan. This creates peer accountability.

Address Defaults Early: If someone misses a payment, address it immediately with the entire group. Delayed action makes recovery harder.

Flexible But Fair: Life happens, crops fail, children get sick, businesses struggle. Show compassion while maintaining accountability. Sometimes, loan restructuring is appropriate.

Pro Tip From The Field: VSLAs with default rates below 5% share one common practice: they discuss every loan application thoroughly before approval. Quick rubber-stamp approvals often lead to problems later.

Handling Conflicts and Challenges

Every VSLA faces challenges. How you handle them determines success or failure.

Common Challenges:

Attendance Problems: Some members become irregular in attendance. Address this quickly, consistent participation is essential for trust.

Payment Defaults: When someone can’t repay, it affects everyone. Create a fair process for addressing defaults that includes understanding circumstances while maintaining consequences.

Leadership Issues: Sometimes leaders abuse their positions or become ineffective. Your constitution should include provisions for removing and replacing leaders if necessary.

Personality Conflicts: Money plus group dynamics can create tension. Address interpersonal issues directly and fairly before they poison the entire group.

Growing Pains: As savings grow, some members may want to change rules, increase loan amounts, or modify meeting frequency. Make changes democratically through proper voting.

Building Group Cohesion

The most successful VSLAs we’ve observed at RDF aren’t just financial arrangements, they’re genuine communities. Build this through:

- Celebrating member milestones (weddings, graduations, business openings)

- Supporting each other during difficulties through the social fund

- Occasional social gatherings beyond regular meetings

- Collaborative projects like group farming or bulk purchases

- Sharing knowledge and helping each other succeed

Connecting Your VSLA to Broader Opportunities

Graduation to Formal Financial Services

VSLAs are excellent starting points, but they’re not the end of your financial journey. As members build savings discipline and business capacity through VSLA participation, many are ready for larger opportunities.

The VSLA-to-RDF Pathway:

Many VSLA members eventually need loans larger than their group can provide, perhaps to expand a successful business, invest in significant farm improvements, or purchase productive assets like dairy cows. This is where institutions like Rural Development Foundation complement VSLAs.

How RDF Supports VSLAs:

- Training: Financial literacy, business planning, and agricultural techniques for entire groups

- Individual Loans: Members can access larger loans while maintaining VSLA membership

- Group Lending: Some mature VSLAs access bulk loans from RDF to expand their collective lending pool

- Agricultural Advisory: Expert guidance to help members improve farming productivity

- Market Linkages: Connections to buyers and suppliers for better prices

VSLA participation actually improves members’ eligibility for RDF loans because it demonstrates savings discipline, financial literacy, and community integration.

Forming VSLA Networks

As your VSLA matures, consider connecting with other groups in your area to form a network or cluster. Benefits include:

- Sharing best practices and learning from other groups’ experiences

- Collective bargaining power for bulk purchases or sales

- Greater political voice for advocating community needs

- Inter-group loans during emergencies

- Joint training and capacity building

RDF facilitates VSLA networks in the Masaka region, providing coordination support and creating opportunities for collaborative projects.

Success Stories: Real VSLAs Transforming Communities

The Kyanamukaaka Coffee Farmers VSLA

Twenty coffee farmers in Kyanamukaaka were trapped in a cycle of poverty. Middlemen paid exploitative prices, and farmers had no capital to improve their farms or process coffee themselves. They formed a VSLA with support from RDF’s community officers.

In their first year, they saved collectively and began providing small loans for coffee pulping machines and improved seedlings. By year two, they had enough capital to bulk-process their coffee and negotiate directly with exporters, increasing their income by 60%.

Today, this VSLA has grown to 35 members, accumulated over 18 million shillings in savings, and operates a small coffee-processing cooperative. Members’ children who were dropping out of school are now completing secondary education.

The Nabugabo Women’s Empowerment Group

Fifteen women in Nabugabo were economically dependent on their husbands with no personal income. They started a VSLA with weekly savings of just 2,000 shillings per member, less than the cost of a kilo of sugar.

Through small loans from their collective savings, members started modest businesses: one bought chickens for eggs, others started vegetable gardens for market sales. As businesses grew, savings increased.

Three years later, every member runs at least one profitable business. The group collectively saves 150,000 shillings per week, and several members have graduated to RDF individual loans for larger investments. Most remarkably, the confidence these women gained has transformed their households, they now participate equally in family decisions and their husbands have become supportive of their economic activities.

The Kalungu Youth Agricultural VSLA

Young people in Kalungu Sub-county faced unemployment with no capital to start businesses or farms. Fourteen young adults (ages 18-25) formed a VSLA focused specifically on agricultural entrepreneurship.

They combined VSLA savings with RDF agricultural advisory services. Members took small loans to start various farming enterprises: mushroom cultivation, poultry, piggery, and vegetable farming. They supported each other with labour during planting and harvesting.

Within 18 months, every member had established a productive farm, and the group had collectively saved 12 million shillings. They used part of their share-out to rent land collectively for a group maize farm, further increasing income. This VSLA demonstrated that young people can succeed in agriculture when given proper support and capital.

Common Mistakes to Avoid When Starting a VSLA in Uganda

Learning from others’ mistakes can save your group significant problems:

Starting Too Large: Groups with more than 30 members become difficult to manage. Keep it manageable.

Complicated Rules: Overly complex constitutions that members don’t understand or can’t follow. Keep rules simple initially.

Lending Too Much Too Soon: Groups that lend most of their savings in early weeks have no cushion for defaults and can’t grow their capital base.

Inconsistent Meetings: Irregular meetings kill momentum and trust. Establish a schedule and stick to it religiously.

Poor Leadership Selection: Choosing leaders based on status rather than skills and trustworthiness. A titled person isn’t necessarily a good treasurer.

No Consequences: Rules without enforcement become meaningless. Apply penalties consistently and fairly.

Ignoring Red Flags: When someone shows signs of financial difficulty or dishonesty, address it immediately rather than hoping it resolves itself.

Insufficient Record-Keeping: Sloppy or incomplete records lead to disputes and loss of trust. Maintain meticulous records from day one.

Financial Literacy: Essential Knowledge for VSLA Members

VSLAs work best when members understand basic financial principles. Here are key concepts every VSLA member should grasp:

The Difference Between Saving and Investing

Saving means setting money aside for future use or emergencies. Your VSLA contributions are savings.

Investing means using money to acquire assets or start activities that generate returns. When you take a VSLA loan to buy chickens that produce eggs for sale, you’re investing.

Both are important, and VSLAs enable both through the same mechanism.

Understanding Interest and Returns

When your VSLA charges 10% interest on a three-month loan of 100,000 shillings, the borrower repays 110,000 shillings. That extra 10,000 shillings is distributed among all members at share-out, meaning everyone’s savings grow beyond their contributions.

This is how VSLAs generate returns, through the small interest charged on loans. The more actively the group lends (while maintaining good repayment), the higher the return at share-out.

Productive vs. Consumption Loans

Productive loans finance activities that generate income: buying farm inputs, purchasing inventory for a business, or acquiring productive assets like sewing machines or wheelbarrows.

Consumption loans finance current needs: school fees, medical bills, food during lean seasons, home repairs.

Both have their place, but groups that emphasise productive loans generally achieve better financial outcomes because these loans help members increase their income, making repayment easier and enabling higher savings in future cycles.

Budgeting and Cash Flow Management

Many VSLA members fail not because they lack income but because they don’t manage cash flow effectively. Basic budgeting skills are essential:

- Track all income and expenses for at least one month

- Identify where money goes and what can be reduced

- Plan purchases rather than buying impulsively

- Separate business money from household money

- Set aside VSLA contributions first before spending on other things

RDF provides budgeting training for VSLAs, contact us to schedule a session for your group.

Your VSLA’s Future: Growth and Sustainability

Typical VSLA Growth Trajectory

Most successful VSLAs follow a similar pattern:

Year 1: Learning phase. Members save modest amounts, take small loans, and learn procedures. Excitement is high, but processes are still being refined. Share-out returns are typically 110-130% of contributions.

Year 2: Maturity phase. Procedures are smooth, trust is established, savings increase. Members take larger loans for more ambitious ventures. Share-out returns reach 130-150%.

Year 3+: Expansion phase. Some members graduate to individual institutional loans while maintaining VSLA membership. The group may take on collective projects. Annual savings can reach millions of shillings.

Signs Your VSLA Is Succeeding

- Consistent attendance above 90%

- Loan repayment rates above 95%

- Increasing savings amounts over time

- Members starting or expanding businesses

- Children staying in school

- Improved household living standards

- Strong group cohesion and mutual support

- Minimal conflicts or disputes

- Growing interest from community members wanting to join

When to Start a Second Group

Once your VSLA reaches maximum membership (25-30 members) and others want to join, consider helping them start a new group rather than expanding beyond a manageable size. Experienced members can mentor new VSLAs, spreading financial inclusion throughout your community.

Getting Support from RDF

At Rural Development Foundation, we’re committed to supporting VSLAs as powerful tools for community transformation. We offer several support services:

VSLA Formation Training

Free comprehensive training for communities wanting to start VSLAs. We cover:

- Complete methodology and procedures

- Constitution development guidance

- Record-keeping systems

- Leadership training

- First meeting facilitation

Ongoing Capacity Building

For established VSLAs:

- Financial literacy workshops

- Business planning training

- Agricultural advisory services

- Group governance strengthening

- Conflict resolution support

Graduation Pathways

When VSLA members are ready for larger financial services:

- Individual agricultural loans (up to 1-year terms with 3-month grace periods)

- Business loans for expanding enterprises

- Education loans for school fees

- Sanitation loans for household improvements

Taking the First Step: Starting Your VSLA Today

The hardest part of starting a VSLA in Uganda isn’t the procedures or the record-keeping, it’s taking that very first step. It’s gathering your members and saying, “Let’s do something different. Let’s build something together.”

You don’t need to wait for perfect conditions or external funding, or government programs. You need commitment, trust, and the willingness to start small. The VSLAs transforming communities across Masaka didn’t begin with a lot of money or sophisticated systems. They began with groups of ordinary people who decided to save together and support each other.

Your Next Steps:

- Identify 10-15 potential members in your community who share your commitment to financial improvement

- Call an initial meeting to gauge interest and explain the VSLA concept

- Contact RDF for free training by calling +256 200912660 or visiting our office at Plot 20 Birch Avenue, Kizungu, Masaka

- Develop your constitution with guidance from experienced facilitators

- Acquire basic materials (lockbox, ledgers, stamps)

- Hold your first savings meeting and celebrate this important beginning

- Maintain consistency through regular meetings and mutual support

We’re Here to Walk This Journey With You

Rural Development Foundation exists to support exactly this kind of community-led transformation. VSLAs embody our core philosophy: that rural communities have tremendous strength and capacity when barriers are removed and proper support is provided.

We’ve helped hundreds of VSLAs across the Greater Masaka region move from initial formation to thriving community institutions. We’ve seen the lives changed, the children educated, the businesses launched, and the dignity restored. We’ve also seen the mistakes that can be avoided and the practices that lead to success.

Our community officers are available to provide training, answer questions, and support your journey toward financial inclusion and community transformation.

The future you dream of for your community doesn’t require external rescue, it requires collective action, mutual support, and the proven methodology of VSLAs. Everything you need is already present in your community: people with dreams, modest resources that become powerful when pooled, and the commitment to lift each other up.

Starting a VSLA in Uganda is one of the most practical, effective, and immediately accessible steps your community can take toward lasting prosperity. The question isn’t whether VSLAs work, decades of evidence across Africa prove they do. The question is: will your community be the next success story?

Let your story begin today.

Need Help Starting Your VSLA?

Contact our community development team to schedule free VSLA formation training for your group. We provide comprehensive support, including constitution development, leadership training, and ongoing mentorship.

Already Have a VSLA?

Learn about financial literacy workshops, agricultural advisory services, and individual loan opportunities for members ready to expand their economic activities.

Additional Resources

Learn More About VSLAs and Financial Inclusion: